Having my own firm gave me the opportunity to make lots of mistakes; and I took advantage of nearly every one of them. Why small architectural firms must be SpartanI saved a blog post titled “The cereal entrepreneur” because it reminded me of a hard-learned lesson. "Cut your expenses to the bone before you need to. Every dollar not spent is a dollar you don’t need to raise. Eat cereal, not sushi. (This is the best reason to start a business when you’re in college).” - Seth Godin https://seths.blog/2018/08/the-cereal-entrepreneur/ During my first few years in business I didn’t say no to many requests to spend money on ...

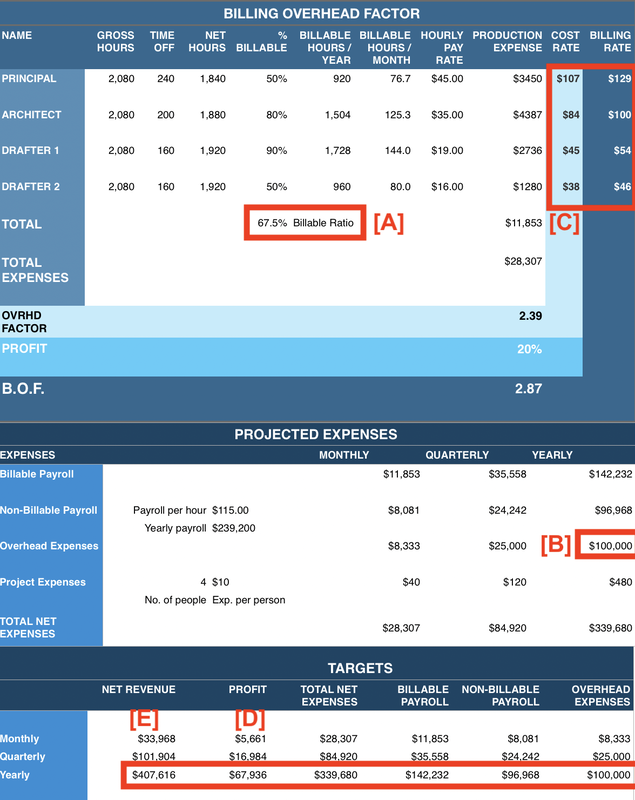

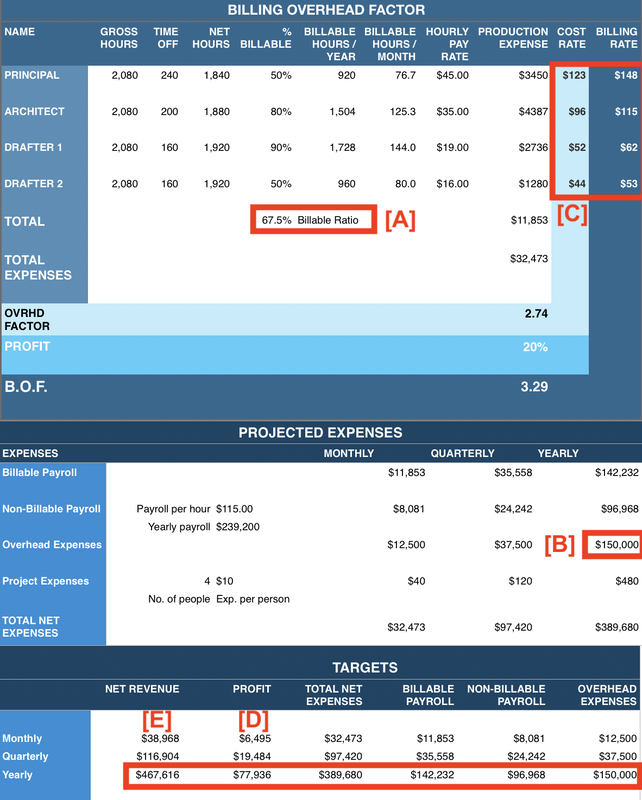

I didn’t like the tight-fisted way previous firms operated. It didn’t go on too long. It shouldn’t have ever started. And walking back the ‘perks’ was painful. It was the first of many hard-learned lessons. (I used to joke that I was earning an MBA the hard way.) We have all experienced some version of Scope Creep and know it is a real thing. Overhead Creep is just as real. It takes constant vigilance to resist Overhead Creep. Here is the damage that it does. The Billing Overhead Factor [BOF] is the only financial model for an architectural firm that I know of. This first BOF has low overhead expenses.  Notice in this BOF above that the Billing Ratio (productivity) is 67.5% [A] and overhead expenses are $100,000 [B] per year for a four person firm. With the labor, charge (cost), and billing rates [C] shown here the firm can make a $67,936 profit [D] on revenue of $407,616 [E]. If they do much hourly work, they very likely can charge 10-20% more per hour because their financial model is very efficient.  In this new BOF the only difference is that the overhead expenses are $150,000 [B] per year instead of $100,000. Now the firm must have revenue of $467,616 [E] to make a profit of $77,936 [D]. It is the same firm working the same hours and with the same productivity. Can they generate the additional revenue or will they give up most of their targeted profit? Notice also what has happened to their billing rates. Hourly work isn’t as beneficial as in the first example. The increased charge (cost) rate means there are fewer hours available for every fixed fee project. At some point the billing rates may become non-competitive. This BOF comparison demonstrates why you want to control the growth of overhead expenses. They make it hard to be viable. You can find out more about Billing Overhead Factors and download the spreadsheets here. [link] I have found that developing a detailed and tight expense budget is enlightening. However, sticking to the budgets is nearly impossible. “In preparing for battle I have always found that plans are useless, but planning is indispensable.” So whether you develop an expense budget or not, the most useful skill is to just say “No” to everything. Occasionally you will want to relent when there is good reason. Request a Cost Benefit Analysis, which is a really helpful skill to develop. At least write down the case for taking on the expense including the pros and cons. Favor things that will save time, demonstrably. If the proposal doesn’t save time, it should be a hard sell. Start out Spartan and challenge every thing every year.  Comments are closed.

|

x

Archives

February 2024

Categories

All

|

Architekwiki | Architect's Resource | Greater Cincinnati

© 2012-2022 Architekwiki

© 2012-2022 Architekwiki